Options, Bitcoin, and Limiting Risk

Derivatives contracts are financial instruments derived from the value of an underlying asset that can offer increased earnings and flexibility but also increased risk. Common derivatives include futures, swaps, and most importantly options.

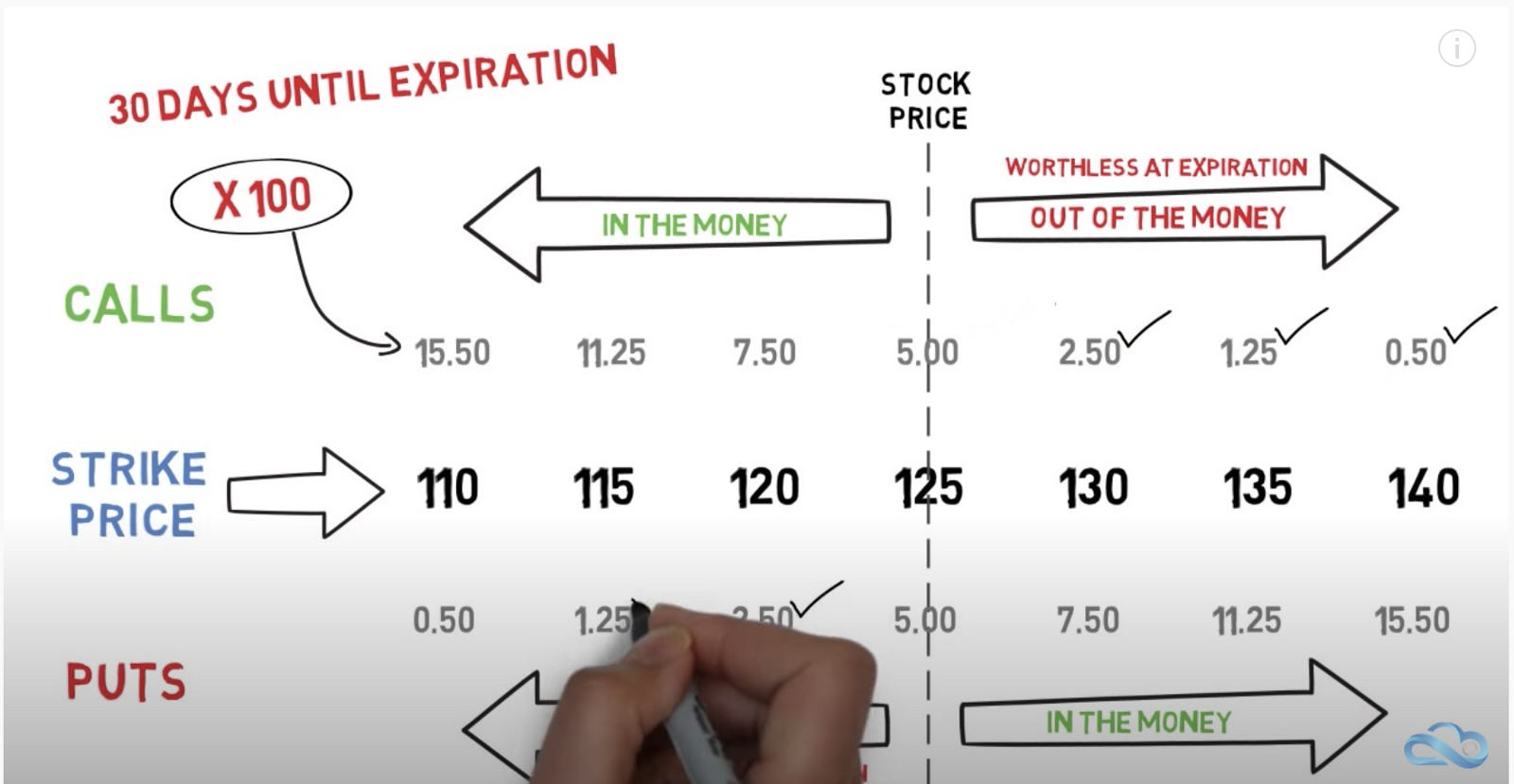

Options contracts allow the owner to speculate on the price of the underlying asset at a fixed date. More precisely, they give the owner the option to buy or sell (depending on the contract type) the underlying asset at a predetermined price (the strike price) on the expiration date. The owner, however, isn’t obligated to do so: they may allow the option to expire without exercising it. There are two types of options contracts, known as call and put options. Calls give the owner the right to buy shares of the underlying asset at the strike price and puts give the owner the right to sell. If a trader buys a call option and the price of the underlying increases to greater than the strike price, the option is said to be in-the-money. If the difference between the current price of the underlying and the strike price is greater than the price paid for the option (the premium), the owner may exercise the option and collect the underlying for a profit. Put options function similarly, except they are in-the-money when the current price decreases below the strike price. The trader will then sell the underlying at the more favorable strike price. If an option is out-of-the-money, the trader will most likely choose to let the contract expire, as it would be preferable to simply trade the underlying at the market price. In this case, only the premium paid for the contract is lost. More succinctly, bullish traders buy call options and bearish traders buy put options.

The opposite is true when writing, or selling, options contracts. A call option writer will profit when the price of the underlying stays below the strike price since they have already collected the premium for the contract and the buyer will choose to let the option expire with any value. Conversely, the seller will lose when the call option expires in-the-money since they will sell the underlying to the buyer for a price lower than the market. The same holds true for put writers, but again in the opposite direction. So selling call options indicates a bearish sentiment, while selling put options indicates a bullish sentiment.

It is important to note that buying calls and selling puts are not equivalent. As the price of the underlying increases, the call buyer’s profit continues to increase (and so does the seller’s loss). But, in the same scenario, a put seller’s profit is capped at the premium. This means that buyers of options contracts have a fixed maximum loss (the premium) but potentially infinite profit, and the opposite is true for sellers. For this reason, some of the most common options trading strategies involve both buying and selling contracts.

So far we have mainly considered a trader buying or selling options and waiting until the expiry. The trader, however, can also trade options with no intent to collect the underlying, and instead focus on the price of the option itself. Being derivatives contracts, options have no intrinsic value (unless they are in-the-money, in which case they effectively assume the value of the underlying) so the premium must be estimated. Perhaps the most famous options pricing formula is the Black-Scholes model. This model uses the current underlying price, the strike price, and the time to maturity (along with the current risk-free interest rate) to calculate the value of an option. For call options, the price increases as the underlying price increases. As the time to maturity decreases, there is less of a chance for the underlying price to move dramatically so the option’s value increases if it is in-the-money, and it decreases if it is not.

In terms of cryptocurrency, several exchanges offer options contracts. Deribit was the first exchange to offer bitcoin options, launching them in June 2016. Boasting by far the most trading activity, the exchange sees $798 million in open interest and $90 million in daily volume as of the current date (February 20, 2020). Deribit also introduced Ethereum options in March 2019, currently with $66 million in open interest and $4.4 million in daily volume. LedgerX launched its bitcoin options in October 2017 and currently has $45 million in open interest, with $670,000 traded daily. OKEx publicly released their bitcoin options in January 2020 but have already accrued $66 million in open interest and $6.5 million in daily volume. Other exchanges with crypto options include CME, Bakkt, IQ Option, and Quedex.

The properties of options contracts make them useful for trading within the blockchain landscape. Since cryptocurrencies tend to be fairly volatile in price, buying options can help maximize potential profits while also limiting losses. For example, bitcoin traded at over $10,000 during mid-September 2019. By the end of the month, it declined to just over $8,000. If a trader bought 10 BTC on September 15, their position would have depreciated by 20% for an empirical loss of $20,000. On the other hand, if they had bought 10 call options with a strike of $11,000 for $100 each on the same date, their options would have expired worthless but their premium was only worth $1,000. If the price of bitcoin instead increased to $12,000 by the end of September, the trader would have gained a profit of $20,000 by holding the asset outright. If they bought the options, they would have had the right to buy the 10 BTC at a discount for $11,000 each. With the $100 premium per contract factored in, they still would have profited but with a lower total return of only $9,000. The decrease in profit is the trade-off for risk protection.

By selling options, a trader may earn what is known as yield. This occurs when the buyer does not exercise the option, and the writer keeps the premium without the obligation to fulfill an unfavorable trade at the request of the buyer. For example, if bitcoin is currently worth $8,000, a trader might consider selling a put option with a strike price of $7,000 for $100. Another trader might buy the option, believing that the price of bitcoin will decrease significantly before the expiration date. As long as the price of bitcoin stays above $7,000 until that date, the buyer will choose not to exercise the option since they could sell the option at market price for a better reward. The writer, therefore, will earn $100 on a risk of $7,000 for a total yield of 1.4%. If this tactic is employed several times per year, it is possible to attain an annualized yield of over 5%.

Despite there being several exchanges on which crypto options are offered, it is still a relatively new domain. Only a handful of firms provide significant amounts of liquidity by market-making, including Akuna Capital, Galaxy Digital, GSR, LedgerPrime, Pattern Research, and QCP Capital. In particular, LedgerPrime is an actively managed quantitative hedge fund, trading digital assets and their derivatives using market-neutral methods. It seeks superior risk-adjusted returns through the use of large data systems and high-frequency trading infrastructure. With over half a century of collective experience in traditional finance, LedgerPrime applies proven investment strategies to the modern scope of cryptocurrency. Few other firms in the space possess these credentials and abilities.

Nobody can be certain of how the market will perform in the future. Especially with an asset as volatile and driven by current events as bitcoin, each day may bring new surprises to its value. However, its price overall has historically tended upwards. And given that the industry is still growing and the technology is rapidly evolving, it is likely that this trend will continue. Bitcoin’s price, though, has certainly experienced sharp declines, such as when the “cryptocurrency bubble” burst at the beginning of 2018 and the currency dropped in value by 65%. Moreover, with the upcoming halving of bitcoin’s block reward, there is much contention regarding its predicted movement throughout the next few months. Call options, with their fixed risk but the unlimited reward in a bull market could be a promising investment approach. The yield provided by selling put options could also attract bullish investors. On the other hand, buying puts and selling calls can hedge against volatile markets and downward movements. Or, with enough capital, a hedge fund such as LedgerPrime can select a strategic balance of all of these instruments to maximize profits and minimize risk. As always, however, only time will tell.